HIGHLIGHTS & IMPLICATIONS:

- Firms sharing a large institutional owner with the ESG rater receive elevated ESG ratings from that rater, especially when the common owner holds a larger stake in the rating agency.

- Higher ratings are linked more to ownership influence and potential conflicts of interest than to genuine ESG improvements, as sister firms with initially high ratings often show poorer future ESG performance and do not receive similarly high scores from unconnected rating agencies.

- There is little evidence supporting investor-activism mechanism. Common owners’ ESG initiatives like shareholder proposals are not associated with higher ESG ratings for sister firms, and this highlights the need to view ESG ratings through an ownership and incentive lens.

Third-party ESG ratings are used in investment practices as key metrics for evaluating corporate ESG performance. However, substantial disagreements in ESG ratings for the same firms across different rating agencies have been documented.

Despite regulatory efforts, it remains crucial to understand how ownership structures affect ESG ratings, especially when there is common ownership between the rater and the rated firm.

Little is known about cross-industry common ownership, such as in cases where institutional investors hold stakes in both ESG rating agencies and the firms they rate. This specific form of common ownership warrants attention, as it could play a role in shaping ESG ratings.

Higher ESG ratings for portfolio companies can benefit common institutional investors by attracting fund inflows and increasing management fees. Therefore, common ownership could be positively associated with ESG ratings.

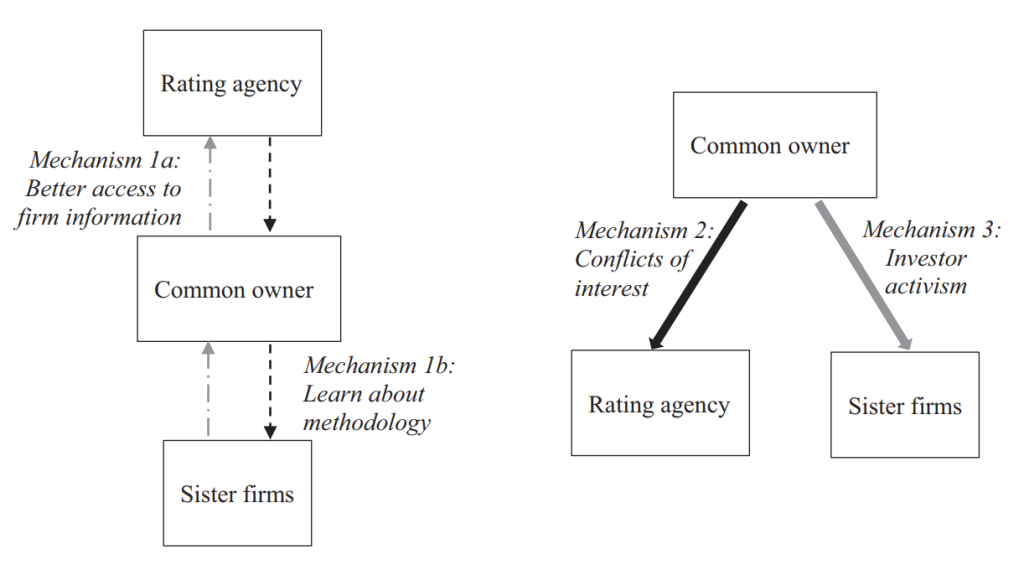

Figure 1

Figure one, above, illustrates three potential theoretical mechanisms through which common ownership between a rating agency and sister firms may influence ESG ratings.

Sister firms are defined as large investee firms owned by a large shareholder of the rating agency during a year. Mechanism 1 involves information sharing, where the rating agency gains better access to firm-specific information through the common owner (mechanism 1a, represented by grey dashed arrowed lines), or where firms learn about the rating agency’s methodology through the common owner (mechanism 1b, represented by black dashed arrowed lines).

In Mechanism 2, depicted with a black solid arrowed line, it shows how the common owner may exert direct influence on the rating agency, potentially leading to conflicts of interest.

In Mechanism 3, shown with a grey solid arrowed line, it represents investor activism, where the common owner engages with sister firms to influence their ESG practices.

In this study, the researchers empirically tested predictions using a large sample of panel data of ESG ratings with information on the major owners of the rated firms and the rating agency. The analysis was based on the ESG ratings from KLD, which provided the most commonly used data in academic research on ESG ratings. Because KLD is part of a publicly listed company, the researchers were able to identify KLD’s institutional shareholders back to 2010. A rated firm was defined as KLD’s “sister firm” if the rated firm and KLD shared the same large shareholder.

The researchers’ analysis provides modest evidence that common owners facilitate information transfer from the rating agency to rated firms, particularly regarding immaterial components used in deriving ESG ratings. They found that the common ownership effect is more pronounced when the common owner holds a larger stake in the rating agency, suggesting influence from the owner on the rater.

The findings are consistent with the notion that the elevated ESG ratings for sister firms are driven by conflicts of interest.

In contrast, ESG ratings from unconnected rating agencies were not associated with KLD sister status. Moreover, sister firms with higher initial ESG ratings tended to have poorer future ESG performance. The findings are consistent with the notion that the elevated ESG ratings for sister firms are driven by conflicts of interest.

Finally, inconsistent with the investor-activism mechanism by which investors engage firms to improve ESG fundamentals, the researchers found that common owners’ ESG pursuits—such as shareholder proposals and UNPRI signatory status—were not associated with higher ESG ratings for sister firms.

This study is the first to examine the common ownership effect on ESG ratings and provides new evidence to understand ESG ratings from the ownership perspective. The study findings of rater-specific high ratings to its sister firms help explain rating disagreement across rating agencies, which is a well-documented phenomenon.

The researchers acknowledged potential limitations in the study, such as the fact that it was based on one rating agency, due to the timing of market development and data availability, given that the ESG ratings market is still young and developing. This study was on the early stage of the market, and the time period available for the research was relatively short, so the researchers cautioned readers about the external validity of the study results.

While the analyses speak to several potential mechanisms— information sharing, conflicts of interest, and investor activism—the researchers did not claim an indisputable conclusion on which channel was ultimately at work. Instead, the findings suggest that mechanisms related to owners’ influence and interest are more consistent with the empirical results.

As the ESG ratings industry matures, more data will become available for further analysis, and future research can address those limitations and yield new insights.

* Learn more from the full research article here:

https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.70016?af=R