1. Introduction

Hong Kong’s global reputation as an international finance and trade hub is now complemented by its aspiration to become a centre for innovation and entrepreneurship. In recent years, the city has undertaken significant efforts to develop its startup ecosystem, supported by policy initiatives, encouraging innovation in its world-class academic institutions, and realigning its position within the GBA.

A quantitative analysis of the evolution of Hong Kong’s startup landscape, including the latest trends and potential future evolution, situating it within the broader GBA and global innovation rankings. The evaluation of the extent to which Hong Kong is capitalising on its advantages is also explored. We find recent startup activity to be muted, but we are optimistic that this is a temporary condition, and the current initiatives are in the right direction. Further steps to accelerate the city’s startup growth and its impact within the region are considered.

Hong Kong’s reputation as a global financial hub is well-established, but its ambitions now extend to innovation and technology. Recent policy initiatives, increased investment in research and development (R&D), and the presence of world-renowned universities have laid the foundation for a potentially vibrant startup ecosystem in the long run.

2. The Size and Trends of Hong Kong’s Startup Ecosystem

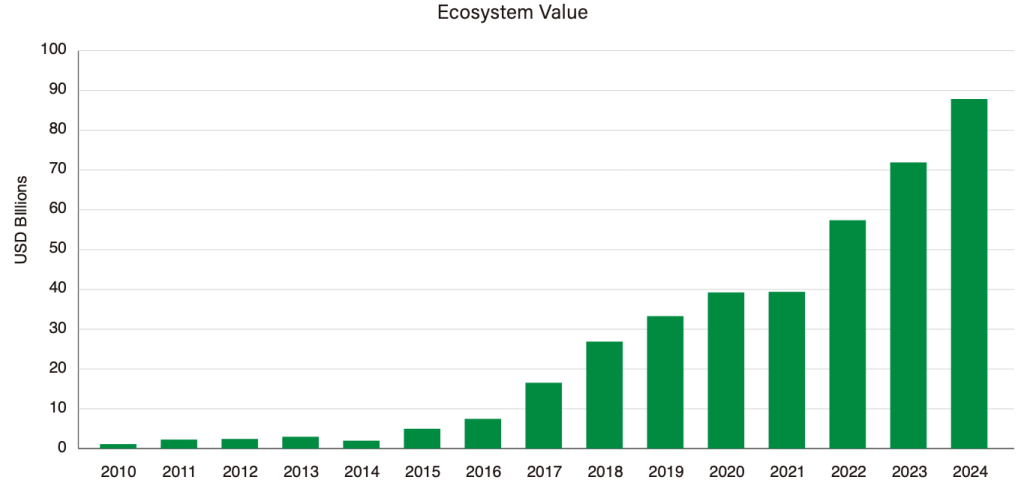

Hong Kong’s startup ecosystem has witnessed substantial growth over the past decade. Startup consultancy Startup Genome[1] has been tracking Hong Kong’s startup ecosystem value (defined as the sum of exit and funding valuations for the prior 2.5 years), and the trend is uniformly and strongly positive (Figure 1).

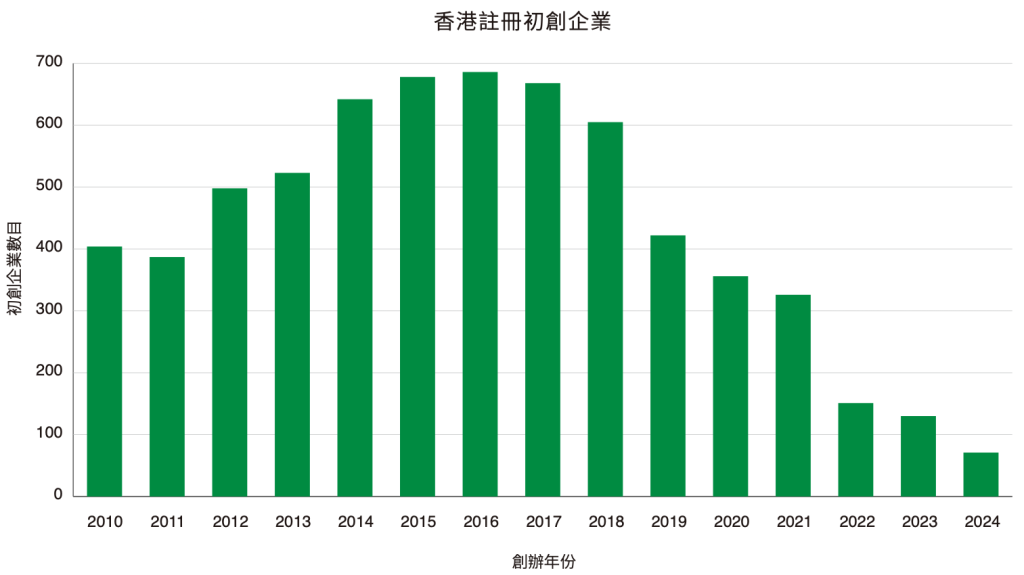

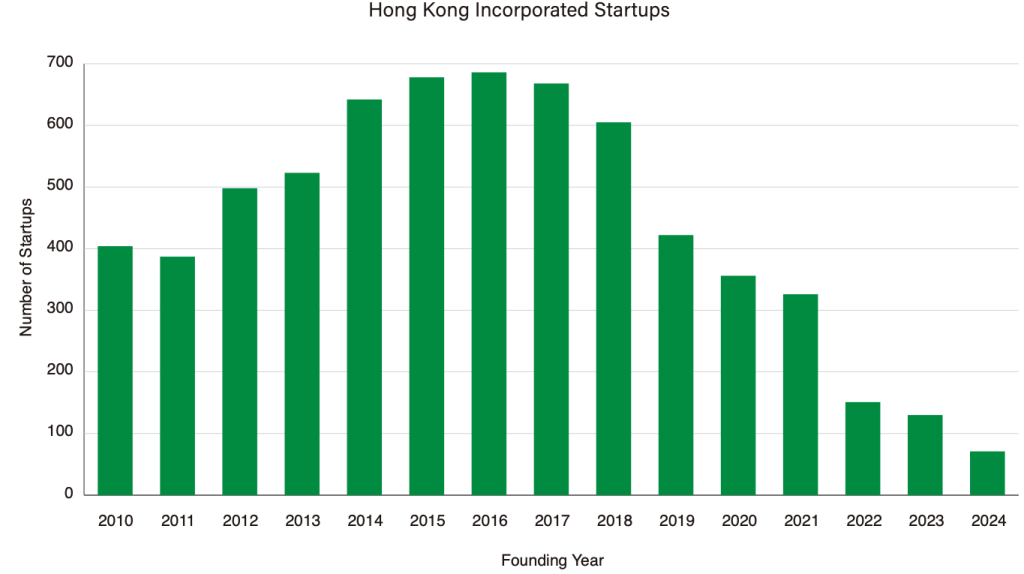

However, this solid performance masks a meaningful slowdown in recent startup activity and vibrancy. Startup data provider Crunchbase[2] shows that the number of startups incorporated in Hong Kong increased sharply from 2010-2018. This growth was supported, as illustrated below, by increased investment activity, a positive global environment for entrepreneurial activity, and favourable government policies, such as the launch of the Innovation and Technology Fund (ITF) in 2015 and the establishment of the Hong Kong Science Park and Hong Kong Cyberport as dedicated innovation hubs.

As Figure 2 indicates, a sharp reversal of this trend can be seen post-2019, mirroring both global trends in venture capital and startup activity and local conditions, including the COVID-19 pandemic, which caused the flow of talents, ideas, and capital to become stagnant.

Figure 1.Hong Kong startup ecosystem value trend is uniformly and strongly positive

Source: Startup Genome

Figure 2.Hong Kong startup formation, 2010-2024

Source: Crunchbase

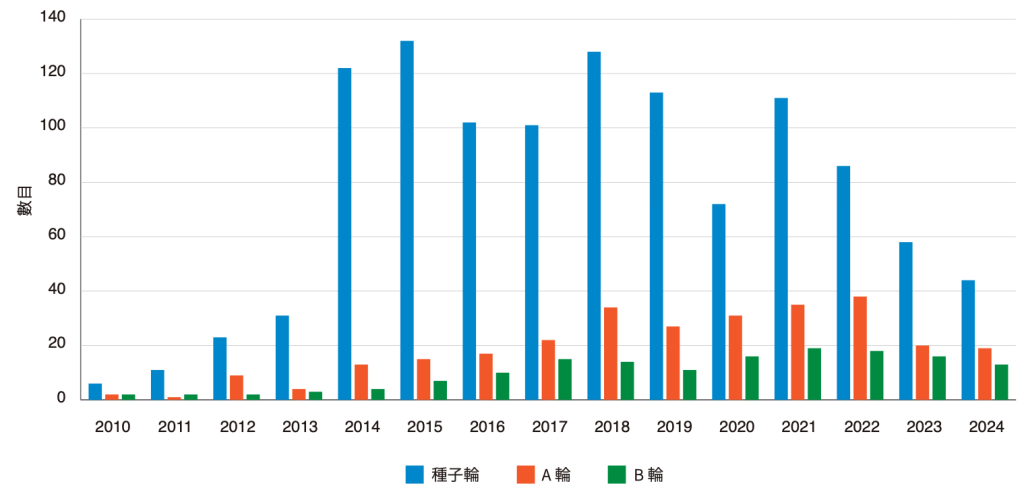

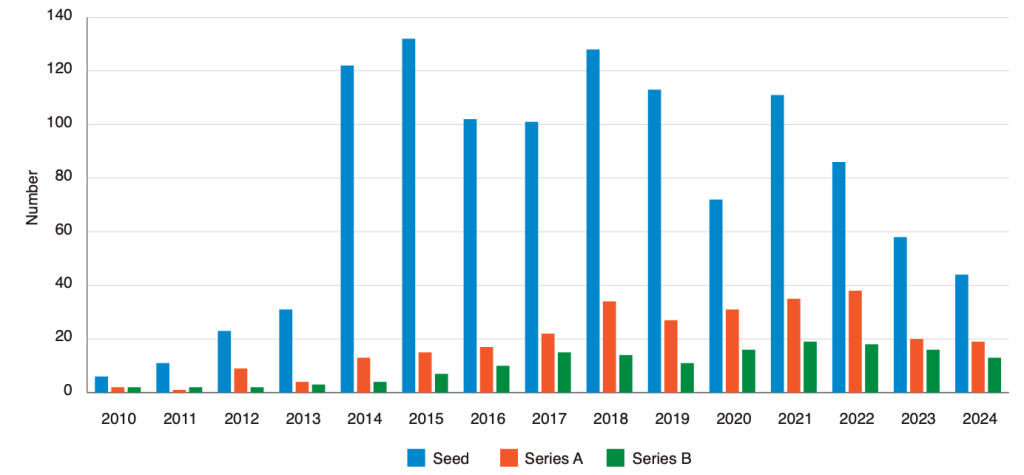

One important caveat of the data points in Figure 2is the material lag in the reporting, so it is very likely that the number of startups incorporated in 2022-2024 is higher than the numbers reported by Crunchbase. However, more complete data from Startup Genome on Seed, Series A, and Series B financings, which represent not startup formation but when they were financed, confirms this slowdown (Figure 3).

Figure 3.Hong Kong Seed, Series A, and Series B financings

Source: Startup Genome

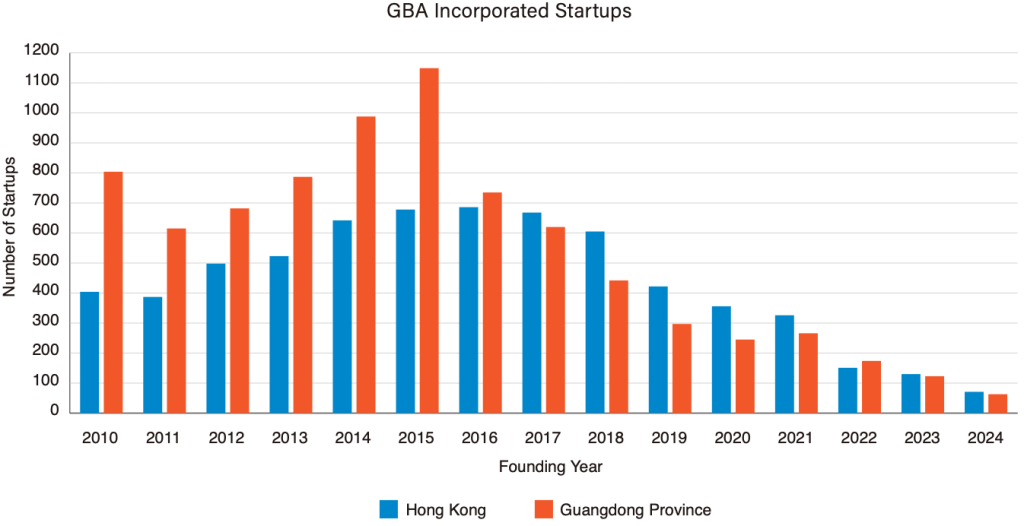

This slowdown does not just affect Hong Kong but extends more broadly to the Greater Bay Area (GBA), as evidenced by Crunchbase data on Guangdong-incorporated startups for the same period (Figure 4). The caveat about the completeness of the Guangdong data also evidently applies, but the trend is quite clear.

Figure 4.Hong Kong and Guangdong Province startup formation, 2010-2024

Source: Crunchbase

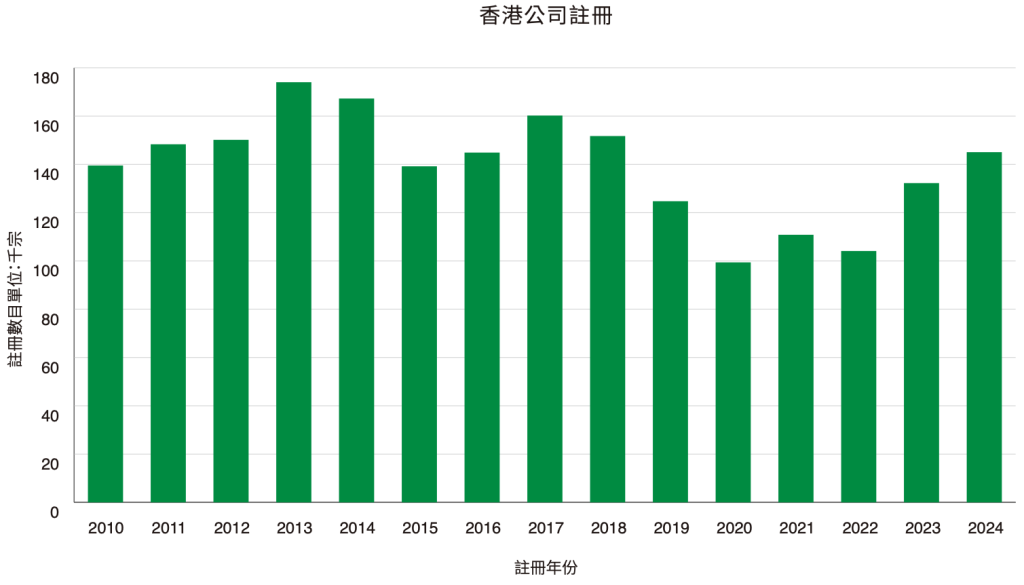

Another possibility is that this decline is part of a broader macroeconomic trend of reduced economic activity in Hong Kong. But this trend in startup formation does not seem to be correlated to general economic activity, as evidenced by Hong Kong Companies Registry data on company registrations. These data, which are a proxy for overall economic dynamism and business formation, show a recovery to close to historical levels in the last couple of years (Figure 5).

Figure 5.Hong Kong company registrations last 15 years

Source: Companies Registry

2.1 Startup Team Size and Scaling Dynamics

The majority of Hong Kong startups remain small, with more than 80% employing fewer than 50 people. Only a handful have scaled beyond 250 employees, a threshold commonly associated with “breakout” growth in the startup world. This pattern reflects the city’s challenges in nurturing and retaining scale-up companies. Local startups often struggle to transition from early success to large-scale operations, hindered by market constraints, funding gaps, and competition from larger regional players.

As Figure 6shows, using Crunchbase data, mature firms are larger. However, focusing on 2014-2018, there is an obvious plateau in startup size, with limits to scale in the Hong Kong startup ecosystem, and the vast majority of mature firms not growing past 50 employees or so.

Figure 6.Evidence in recent years of limits to scale in startup size

Source: Crunchbase

2.2 Investment, Financings, and Exits

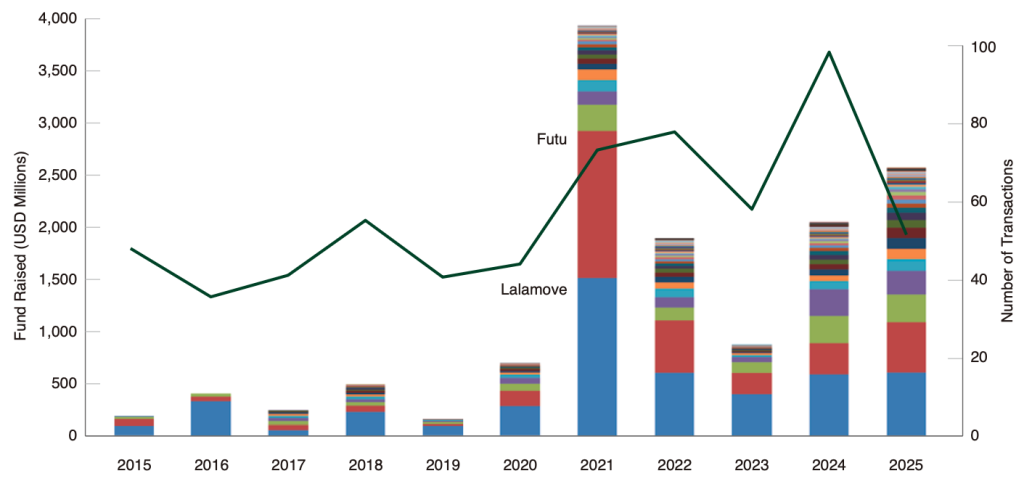

In contrast to the recent rates of startup formation, the financing and funding environment in Hong Kong remains robust. The number of financing transactions had been rising, with a decline in deal size in 2022-2023, which is in line with the global startup financing environment, followed by a strong rebound in financing activity in 2024 and 2025 YTD (Figure 7).

Figure 7.Hong Kong financing numbers and amounts

Source: Crunchbase

Seed and early-stage funding remain relatively accessible, supported by government grants and angel investors, but growth-stage and late-stage capital are scarce—this is a critical bottleneck for startups seeking to scale (see Figure 3).

Hong Kong has produced a handful of unicorns and high-value startups, including Futu (digital finance), Lalamove (logistics), and SenseTime (AI). However, these successes are relatively rare, and several of Hong Kong’s highest-profile startups have faced stiff competition from the Chinese M ainland and international rivals. This is also apparent in the number of exits, which has been declining over the last few years in line with the reduced rate of startup formation, as shown in Figure 8.

Figure 8.Startup exit declines in the city

Source: Startup Genome

2.3 Startups across Sectors

From our dataset covering over 10,000 enterprises incorporated in Hong Kong in the past 10 years, we can see the key trends across sectors and how they reflect policy drivers, as well as local and global events (Figure 9). A good example is during the COVID-19 pandemic which hindered businesses related to physical interaction but empowered digital transformation across industries.

Overall, steady contributions to the field have been from the traditional sectors such as Manufacturing & Industrial, Media & Entertainment, Consulting & Professional Services, Retail & e-Commerce, Logistics & Supply Chain Management, Healthcare & Life Sciences, Education & Ed-tech, NGOs, and others. Among those, Software & Internet and Financial Services have been the key sectors delivering higher numbers of startups. It is worth noting that the numbers for blockchain and artificial intelligence (AI) have been rapidly rising.

From the dataset analysis, our forecast would be threefold: 1. traditional sectors are the areas where there will be high demand for digital transformation; 2. our strength in Internet-related and financial services, especially as it will empower and be empowered by cross-border business; and 3. the latest wave of emerging technology, including AI and blockchain.

Figure 9.Startup figures and trends across sectors in the past 10 years

Source: Crunchbase

3. Hong Kong and the GBA in the Global Innovation Landscape

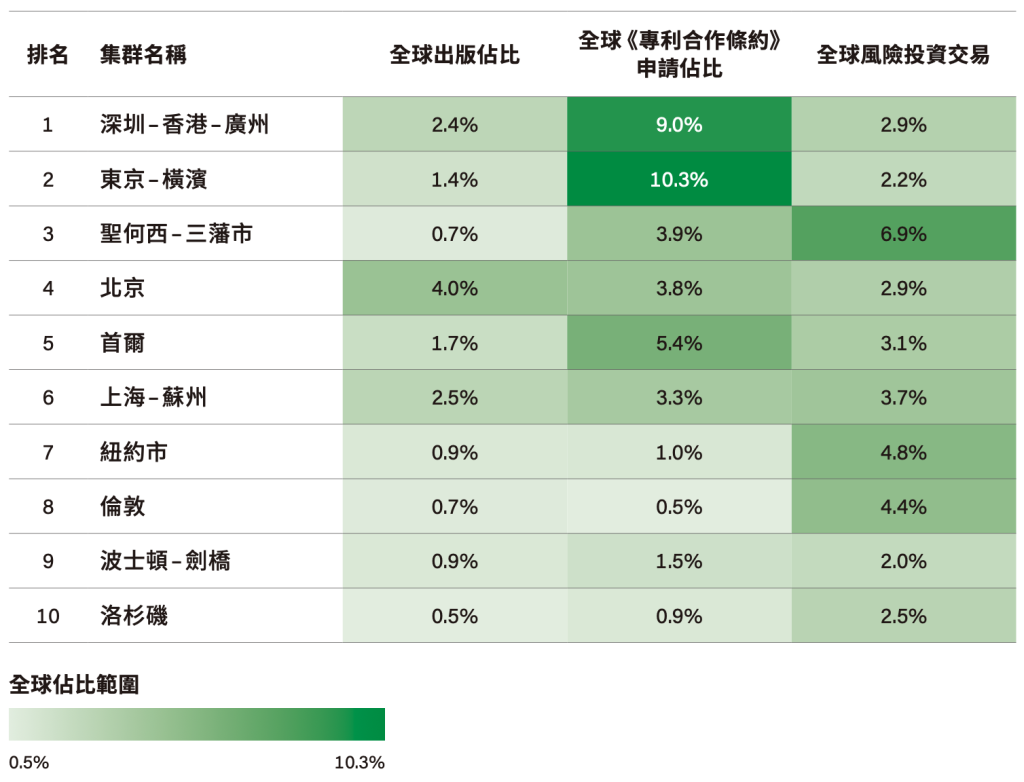

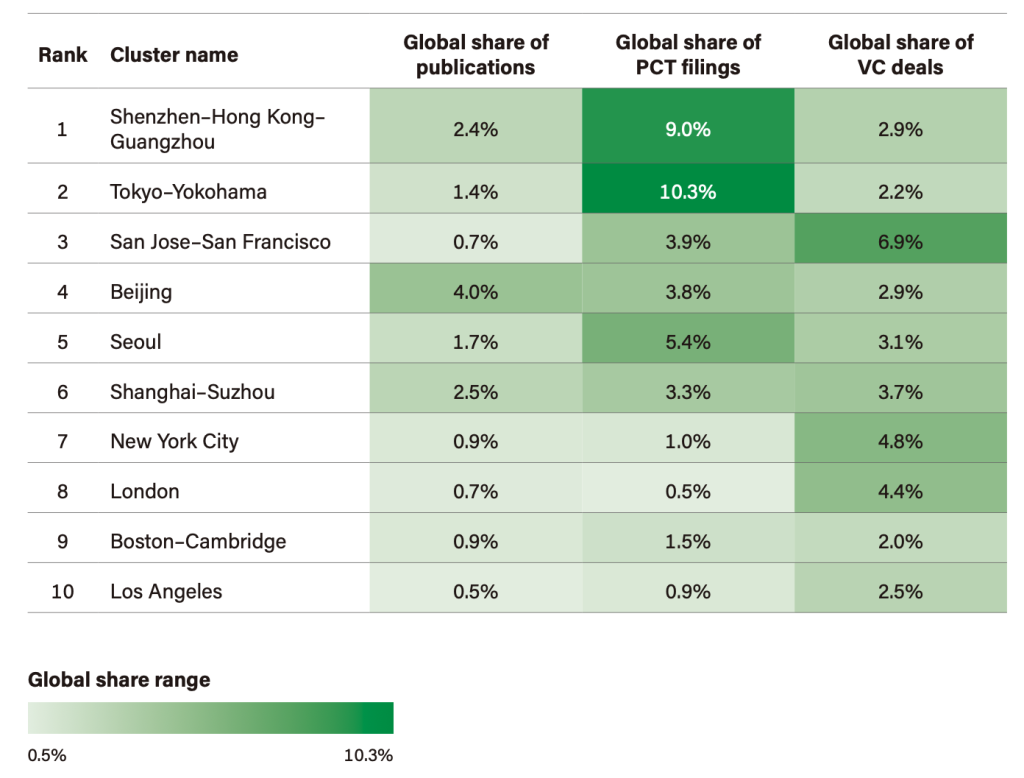

Taking a historical view of the role of Hong Kong in the GBA, the city has been and will continue to be an important contributor to the regional ecosystem. The Shenzhen-Hong Kong-Guangzhou cluster ranks #1 globally in the WIPO Global Innovation Index 2025, contributing 2.4% of global academic publications and 9–10% of PCT patent filings (Figure 10).

Despite this, Hong Kong’s and the GBA’s per capita innovation output trails leading clusters such as Cambridge (UK) and San Jose (USA). According to the OECD, Hong Kong produces 1.2 PCT applications per 1,000 residents, compared to 3.8 in Cambridge and 4.2 in Silicon Valley. This gap underscores the challenge of converting research excellence into commercially viable startups and sustained innovation.

Figure 10.GBA ranks #1 globally in the WIPO Global Innovation Index 2025

Source: WIPO Statistics Database, May 2025

3.1. Hong Kong and its GBA Peers

According to PitchBook, between Q3 2018 and Q2 2024, Hong Kong startups secured US$16.6 billion in financing, accounting for a significant share of the US$83 billion total deal value in the GBA (Figure 11). While this demonstrates Hong Kong’s strong position as a regional financial centre, it is notably less than the US$41.8 billion raised by Shenzhen startups during the same period. This disparity highlights Hong Kong’s shifting secondary role within the GBA’s innovation cluster, particularly in terms of deep-tech and large-scale technology financing, but points to shifting trends that could be leveraged to the benefit of Hong Kong and GBA ecosystems.

Figure 11.Hong Kong and GBA startup ecosystem

Source: PitchBook, all data Q3 2018-Q2 2024

Hong Kong’s startup exit values between 2018 and 2024 totalled US$29.7 billion (Figure 10), again trailing Shenzhen’s US$72.9 billion , which suggests that while the city provides robust exit opportunities, particularly through its stock exchange, it has yet to establish itself as the premier destination for tech startup IPOs or mergers and acquisitions in the region.

Quantitative comparisons reveal that although Hong Kong’s startup formation has grown over the past decade, cities such as Shenzhen and Guangzhou have outpaced it both in the number of startups and in total secured financing. These cities have leveraged their extensive supply chain networks, advanced manufacturing capabilities, and deep pools of tech talent to nurture a vibrant ecosystem of rapidly scaling technology companies.

Ultimately, Hong Kong’s role within the GBA remains distinctive. It continues to serve as a gateway for international capital and legal structuring, leveraging its common law system and status as a global financial centre. However, its contribution to rapid technology scaling, especially in sectors such as deep tech and advanced manufacturing, is currently less pronounced compared to Shenzhen’s robust platform companies (e.g., Tencent, Huawei and DJI), which provide extensive supply and industry support to local startups. We believe this is an opportunity for Hong Kong to step in and contribute to the GBA startup ecosystem.

4. Key Policy Recommendations

As mentioned earlier, the slowdown in Hong Kong startup formation and activity is due to both changes in the macroeconomic environment and a structural shift in the region’s startup ecosystem towards the GBA. This transition period presents an opportunity to realign and reinvigorate the combined ecosystem in a more organised and productive way. In this section, we describe potential initiatives to drive this realignment.

4.1 Better Aligned Sector and Vertical Orientation

Hong Kong’s startup ecosystem is strongly represented in fintech, logistics, and digital finance, leveraging the city’s established financial infrastructure and trade networks. Companies like Lalamove (logistics) and Futu (digital finance) exemplify this trend.

But competition is intensifying, and to maintain its edge, Hong Kong must diversify into emerging sectors such as AI, green technology, and health tech. According to Startup Genome, AI and data analytics ventures in Hong Kong grew by 35% annually between 2020 and 2023, while health tech saw a 28% increase. Despite these gains, the ecosystem remains less diversified than top global hubs, and therefore, more support is needed for deep tech and advanced manufacturing.

Acknowledging that Hong Kong’s domestic market is limited by its population size and geography, startups must quickly access regional or international markets to achieve scale. This requires sophisticated market understanding and a global business model design. High costs—especially for office space, housing, and talent—raise barriers for early-stage founders and increase the risk profile for investors.

Recent trends, such as the rise of Real World Asset (RWA) tokenisation and digital finance, highlight Hong Kong’s potential to lead in financial innovation and regulatory technology (regtech). By aligning fintech development with legal and compliance expertise, Hong Kong can simultaneously attract overseas investment and support GBA corporates in business transformation.

4.2. Stronger Internationalisation and Talent Acquisition

Hong Kong positions itself as a global hub for international founders and venture capitalists, benefiting from its open economy, robust legal protections, and world-class connectivity. While the city attracts talented students from the Chinese Mainland and abroad—especially to its world-renowned universities—retaining these talents after graduation remains a challenge. Many STEM graduates and high-tech professionals seek opportunities in the Chinese Mainland or other regional centres, attracted by larger markets and more vibrant startup ecosystems.

According to the Hong Kong government’s 2023 labour statistics, 32% of STEM graduates seek employment outside Hong Kong, primarily in the Chinese Mainland, Singapore, and the United States. The Hong Kong government’s 2025 Policy Address emphasised increasing the number of non-local students at local universities, but there is a pressing need for enhanced career support and clear pathways for these graduates to anchor their innovation and R&D activities within Hong Kong and GBA ecosystems.

4.3. Rethinking the Financing and Exit Environment

While seed and early-stage funding are relatively accessible in Hong Kong, there is a pronounced scarcity of growth-stage and late-stage capital compared to tech hubs in Silicon Valley or Shenzhen. This funding gap impedes a startup’s ability to scale, invest in R&D, and compete internationally.

Growth-stage and late-stage funding remain major bottlenecks, with institutional investors in Hong Kong, such as pension funds and insurance companies, allocating only a small fraction of their portfolios to venture capital and private equity. This is in contrast to Silicon Valley, where institutional venture capital investment is a cornerstone of ecosystem scale-up.

Hong Kong’s stock exchange offers robust IPO and M&A opportunities, but it is perceived as less attractive for high-growth technology startups than the US NASDAQ or Shanghai’s STAR Market. As a result, some of the city’s most promising ventures seek exits or secondary listings abroad, diluting the impact of local innovation.

Exit options are robust in financial and logistics sectors, but the Hong Kong Stock Exchange is perceived as less attractive for deep-tech and high-growth technology IPOs. The regulatory environment, while stable, is seen as less flexible than the US or Chinese Mainland markets. Consequently, several promising Hong Kong startups have sought exits or secondary listings elsewhere.

4.4. Better Alignment Between Early-Stage Innovation and Market Environment

Despite the presence of world-class universities and research institutes, Hong Kong’s per capita scientific output and patenting activity remain below those of leading global innovation hubs. This gap limits the pipeline of deep tech ventures and reduces the ecosystem’s capacity to generate high-impact startups. Furthermore, relatively few startups transition from small teams to large employers or ‘unicorns’, indicating challenges in business model scalability and market adoption.

Two areas are suggested as the focus for innovation and technology development in Hong Kong. First, while Hong Kong has a strong international university cluster and robust R&D from academic and research institutes, the ecosystem lacks market understanding—locally, nationally, and globally—as well as insight into investment trends. Business model design and planning that enable projects to scale up could be aligned to allow early coordination between industry, academia, and policy guidance to unleash startup potential.

Second, the availability of a flexible and deep industry and supply chain has been key to rapid innovation and technology development in the Chinese Mainland. Hong Kong needs to support startups in connecting to the supply chain and industry chain in the GBA as a critical step for project implementation and advanced manufacturing, as well as supporting Chinese corporates in their overseas expansion strategies.

4.5 Closing the Gap Between Academia and Market Needs

Hong Kong has several top global universities with strong research output in both quality and quantity. However, to achieve successful technology transfer and market penetration, there needs to be market research on industry pain points and user requirements, converting research into market demand.

Early industry involvement could play a key role. In China, BAT (Baidu, Alibaba, Tencent) are giants not only because of their market share, but also because they have empowered new startups through investments and resources. These companies’ platforms, user bases, and data have helped startups establish themselves. New big-tech platforms such as Pinduoduo, Meituan, and Bytedance (Tiktok), as well as advanced AI and robotics companies like Game Science, DeepSeek, Unitree Robotics, DEEP Robotics, BrainCo, and Manycore Tech, have become important players.

The focus is not only to attract these companies to establish operations and business through Hong Kong, but also to encourage them to incubate local startups. Through collaboration with these large corporates, Hong Kong startups and innovation projects could gain access to a more complete ecosystem and comprehensive resources, beyond just financial support.

4.6 Closing the Knowledge Gap Between Hong Kong Startups and the Mainland Market

Both startups and established businesses, including corporates and SMEs, face the challenge of Hong Kong’s market being too small to sustain or scale their businesses. The Chinese Mainland market, particularly the GBA, is the key target after proof-of-concept is achieved in Hong Kong.

There are cultural and user behaviour differences. Most products and services—including digital marketing strategies—cannot be directly transferred across the border. Many businesses are unaccustomed to the Chinese Mainland business environment. It is critical that businesses learn about the Chinese Mainland market, especially the GBA, and develop the mentality and capability to adapt their products, services, business models, logistics, and marketing accordingly.

4.7 Closing the Knowledge Gap Between Hong Kong Startups and the Global Market

Hong Kong has long been the direct channel between China and the rest of the world, with its robust financial and legal system and the “One Country, Two Systems” policy. The innovation ecosystem in Hong Kong has to play this role now more than ever. There are two key needs: First, local startups need to better understand international trends, standards, investment flows, and regulatory environments to inform their long-term business scaling plans. Second, Hong Kong businesses should further establish themselves as a catalytic force in the value chain of innovation projects across industries, positioning Hong Kong as a global innovation gateway connecting China’s domestic supply chain with global markets.

This aligns with national policy directions such as the Belt & Road Initiative, as well as expansion into Africa and Latin America. These efforts can be supported by research and insights from research institutes, trade departments, and local trade associations.

4.8 Providing Value-Added Services that Play to Hong Kong’s Strengths

A strategic direction for Hong Kong would be to develop “innovation services” within the value chain. This could be possible if Hong Kong aligns its innovation and entrepreneurship development plan by leveraging China’s strength in domestic industrial supply and value chains.

While manufacturing is concentrated in the Chinese Mainland, Hong Kong can provide creative and professional services—such as design, IP management, finance, and legal support—as high-value services for innovation projects. Supply-chain finance and serving as a hub for attracting foreign capital can further strengthen Hong Kong’s position as an international financial centre. In the long term, Hong Kong should foster talent development related to supply chain and value chain innovation, including industrial digitalisation and entrepreneurial engineering. This can be achieved through relevant program development and training collaborations with industry.

4.9 Integrating the Northern Metropolis and Startup Development Policies

In the Chief Executive’s 2025 Policy Address, significant attention was given to the development and acceleration of the Northern Metropolis, particularly regarding the establishment of a dedicated working group, the streamlining of administrative procedures, and infrastructure development. Alongside the focus on attracting research talent and the aim to establish an international innovation and technology centre, these initiatives set the stage in terms of hardware and software for promoting innovation and entrepreneurship.

Hong Kong has extensive experience in urban planning and infrastructure development, especially with previous satellite towns in the New Territories; relatively recent examples being Tuen Mun, Tseung Kwan O, and Tin Shui Wai. In the areas of research and development, the Hong Kong government has a strong track record of supporting university-based research but these efforts require more collaboration to fully unlock the potential of the Northern Metropolis.

To ensure the success of the Northern Metropolis, planning must be aligned with the goal of establishing it as an innovation centre, and this requires the engagement of several critical stakeholders in addition to those already involved.

First and foremost, strong engagement with industry players is essential. A key aspect of innovation is market implementation and scaling-up, which means that industry presence—including their supply chain and value chain—must be integrated. This involves more than just offices and laboratories; it requires the formation of clusters of related sectors and businesses. Corporate participation in R&D can improve commercialisation rates and facilitate mass production and market adoption, bridging a critical gap for many startups in Hong Kong. These efforts can be further supported by developing a robust industry feedback and insight response mechanism.

Despite these initiatives, the Northern Metropolis within Hong Kong remains limited in terms of available land. Therefore, integration with Shenzhen and within the GBA is both necessary and imminent. Increased cross-border coordination will allow for optimal use of resources, including land, enabling efficient co-development between Hong Kong and Shenzhen. This can be further enhanced through consistent policy alignment and a unified governance framework, which could be extended beyond the Northern Metropolis to include the greater region, all the way to Qianhai.

[1] https://startupgenome.com/. The authors thank Startup Genome and JF Gauthier, CEO & Founder, for providing proprietary data for benchmarking Hong Kong’s startup ecosystem, used with permission.